Managing Your Budget

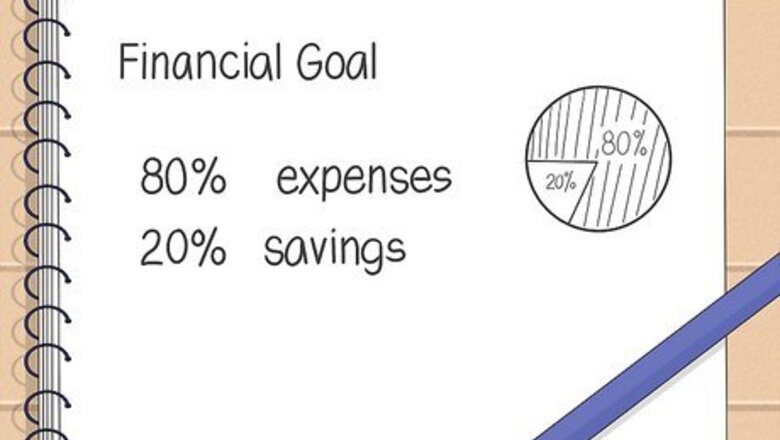

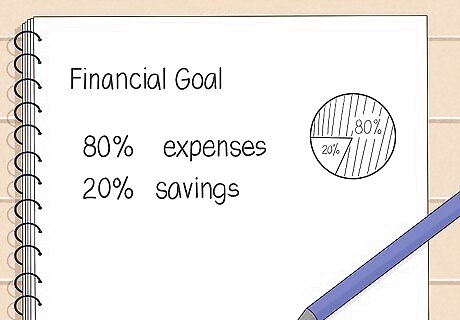

Set your financial goals. Understanding what you are working toward will help you build a budget to meet your needs. Do you want to pay down debt? Are you saving for a major purchase? Are you just looking to be more financially stable? Identify your top priorities so that you can build your budget to fit them. For instance, you might set a goal to save 10% of your income. For a more aggressive savings goal, go for the 80-20 rule, where you save 20% of your income.

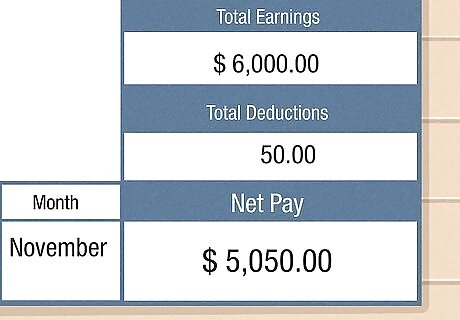

Look at your overall monthly income. A smart budget is one that doesn’t overextend your means. Start by calculating your total monthly income. Include not just the money you get from work but any cash you get from things like side-hustles, alimony, or child support. If you share expenses with your partner, calculate your combined income to figure out a household budget. You should aim to have your overall monthly spending not exceed what you bring in. Emergencies and unforeseen occasions happen, but try to set a goal of not using your credit card to cover non-necessary items when your bank balances are low.

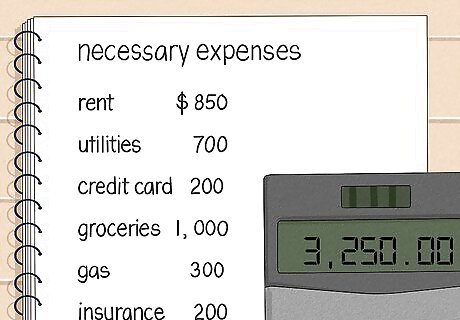

Calculate your necessary expenses. Your first priority in building a better budget should be those things that need to be paid every month. Paying these expenses should be your first priority, as these items are not only necessary for daily activities but could also damage your credit if you fail to pay them in full and on time. Such expenses may include your mortgage or rent, utilities, car payments, and credit card payments, as well as things like your groceries, gas, and insurance. Set up your bills on autopay to make them easy to prioritize. This way the money comes out of your account on the day the bill is due. Set up autopay only if you're sure you'll have enough money each month to pay those bills in full.

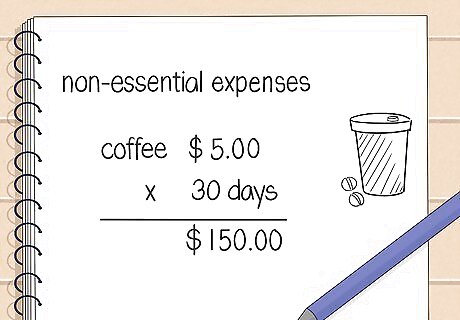

Factor in your non-essential expenses. Budgets work best when they reflect your daily life. Take a look at your regular, non-essential expenses, and build them into your budget so that you can anticipate your spending. If you get a coffee every morning on the way to work, for example, throw that into your budget.

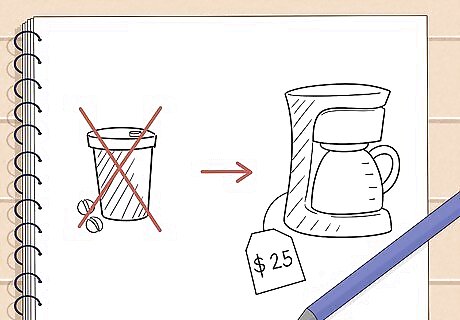

Look for places to make cuts. Creating a budget will help you identify things you can cut from your regular expenses and roll into your savings or debt payments. Investing in a good coffee pot and a mug, for example, can help you save on your morning fix for years to come. Don’t forget your longer-term expenses. Check things like insurance policies, and see if there are places you can scale back. If you are paying for collision and comprehensive insurance on an old car, for example, you may opt to scale back to liability insurance only.

Track your monthly spending. A budget is a guideline for your overall spending habits. Your actual spending will vary each month depending upon your personal needs. Track your spending by using an expenses journal, a spreadsheet, or even a budgeting app to help you ensure that you are staying within your means each month. If you do exceed your budget goals, don’t beat yourself up. Use the opportunity to see if you need to revise your budget to include new expenses. Remind yourself that getting off-target happens to everyone occasionally and that you can still get to where you want to be.

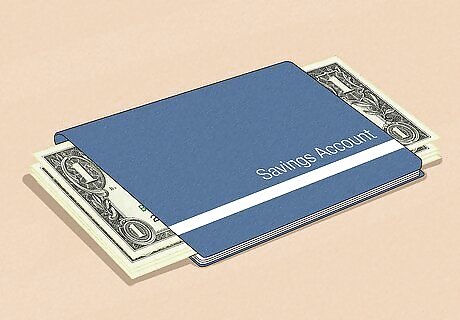

Build some savings into your budget. Exactly how much you save will depend upon your job, your personal expenses, and your individual financial goals. Aim to save something each month, however, whether it’s $50 or $500. Keep that money in a savings account separate from your primary bank account so that it doesn't accidentally get spent. This savings should be separate from your 401(k) or any other investments that you have. Building a small general-savings balance will help you protect yourself financially if an emergency comes up, such as a major repair on the house or unexpectedly losing your job. Many financial experts recommend a target savings of six months’ worth of expenses. If you have a lot of debt you need to pay down, aim for a partial emergency fund of two months' expenses. Then focus the rest of your cash on your debt.

Paying Off Debts

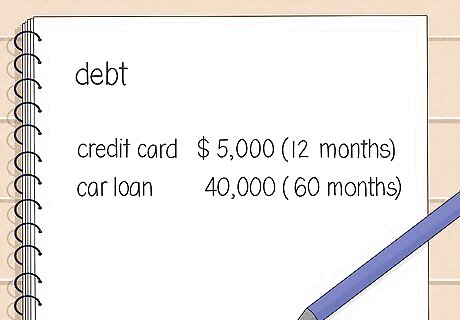

Figure out how much you owe. To understand how best to pay down your debt, you first need to understand how much you owe. Add together all your debts, including credit cards, short-term loans, student loans, and any mortgages or auto financing you have in your name. Look at your total debt numbers to help you understand how much you owe and how long it will realistically take to pay it off.

Prioritize high-interest debts. Debts like credit cards tend to have higher interest rates than things like student loans. The longer you carry a balance on high-interest debts, the more you ultimately pay. Prioritize paying down your highest-interest debts first, making minimum payments on other debts and putting extra money into your top debt priorities. If you have a short-term loan (a car loan, for example), pay that down, too, as quickly as possible. Such loans can become very expensive if not paid off in full and on time.

Go straight from paying off your highest-interest debt to paying off your next-highest-interest debt. When you pay off a credit card balance, don’t roll that payment amount back into your discretionary funds. Instead, roll the amount you were paying into your next debt. If, for example, you finish paying off a credit card, take the amount you were putting toward that card and add it to the minimum payment you've been making on another card or a student loan. The point is that you want to eliminate all recurring, long- and short-term debt as soon as possible so that you can live interest-free.

Setting Up Savings

Pick a savings goal. Saving tends to be easier when you know what you’re saving for. Try to set a goal, such as building an emergency fund, saving for a down payment, saving for a major household purchase, or building a retirement fund. If your bank will let you, you can even give your account a nickname such as “Vacation Fund” to help remind you of what you’re working toward.

Keep your savings in a separate account. A savings account is generally the easiest place to put your savings if you are just starting out. If you already have a solid emergency fund and have a reasonable amount to invest, such as $1,000, you may consider something like a certificate of deposit (CD). CDs make your money much harder to get to for a fixed period of time but tend to pay you a higher interest rate. Keeping your savings separate from your checking account will make it less likely that you'll spend your savings. Savings accounts also tend to pay a slightly higher interest rate than checking accounts. Many banks will allow you to set up an automatic transfer between your checking and savings accounts. Set up a monthly transfer from your checking to your savings, even if it’s just for a small amount. That's a relatively painless way to build your savings.

Invest raises and bonuses. If you get a raise, a bonus, a tax refund, or an unexpected windfall, put it in your savings or, if you have one, your retirement account. This is an easy way to help boost your account without compromising your current budget. If you get a raise, invest the difference between your budgeted salary and your new salary directly into your savings. Since you already have a plan to live off your old salary, you can use the new influx of cash to build your savings.

Dedicate any additional income to your savings. If you work a side gig or if you have any extra sources of income, build a budget based on your primary source of income, and dedicate your other earnings to your savings or retirement account. This will help grow your savings faster while making your budget more comfortable.

Spending Money Wisely

Prioritize your needs. Start each budget period by paying for your needs. This should include your rent or mortgage, utility bills, insurance, gas, groceries, recurring medical expenses, and any other expenses you may have. Do not put any money toward non-essential expenses until all of your necessary living costs have been paid.

Shop around. It can be easy to get in the habit of shopping in the same place repeatedly, but taking time to shop around can help you find the best deals. Check in stores and online to look for the best prices for your needs. Look for stores that might be running sales or that specialize in discount or surplus merchandise. Bulk stores can be useful for buying things you use a lot or things that don't expire, such as cleaning supplies.

Buy clothes and shoes out-of-season. New styles of clothing, shoes, and accessories generally come out seasonally. Shopping out-of-season can help you find better prices on fashion items. Shopping online is particularly useful for out-of-season clothes, as not all stores will have non-seasonal items.

Use cash instead of cards. For non-necessary expenses such as going out to eat or seeing a movie, set a budget. Withdraw the necessary amount of cash before you go out, and leave your cards at home. This will make it more difficult to overspend or impulse buy while you're out.

Monitor your spending. Ultimately, as long as you're not spending more than you bring in, you're on target. Regularly monitor your spending in whatever way works best for you. You may prefer to check your bank account every day, or you could sign up for a money-monitoring app such as Mint, Dollarbird, or BillGuard to help you track your spending.

Comments

0 comment