The Budget 2021 was the most important budget of the NDA government, set as it was against an exogenous shock from a “black swan” pandemic that locked down the economy, stifled economic growth, suppressed tax revenues, and demanded ever-increasing expenditures for recovery. The ‘trilemma’ before the finance minister was how to restore the economy to its pre-Covid trajectory, while enabling the recovery of people and economy hurting from the loss of livelihoods, supply and demand, and creating a new trajectory of resurgence. Not easy during normal times; a nearly hopeless expectation during an economic free fall.

While economists the world over for once agreed that fiscal deficit is not a primary concern and that large expenditures would be required to restore the battered economies, some naysayers did ask where the money would come for the expenditure, little realising that at the end of the day a fiscal deficit is a notional loss, especially as the country finances it through issuing or printing more currency. But the entrenched economic dogmas concerning “fiscal discipline” ensured that, over the years, the notional has become real and the real has paralysed systems and expenditures.

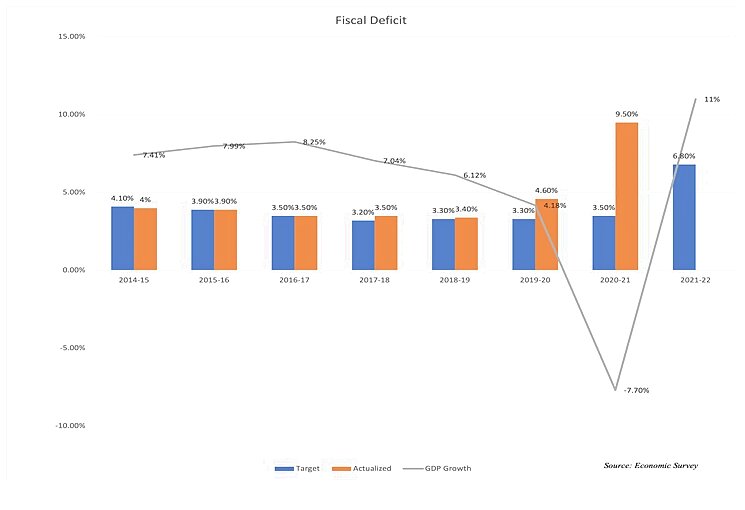

From this perspective, the admission of fiscal deficit being at nearly 9.5% itself took a lot of courage and effort from the government.

Uncharted Territory

RESTORE

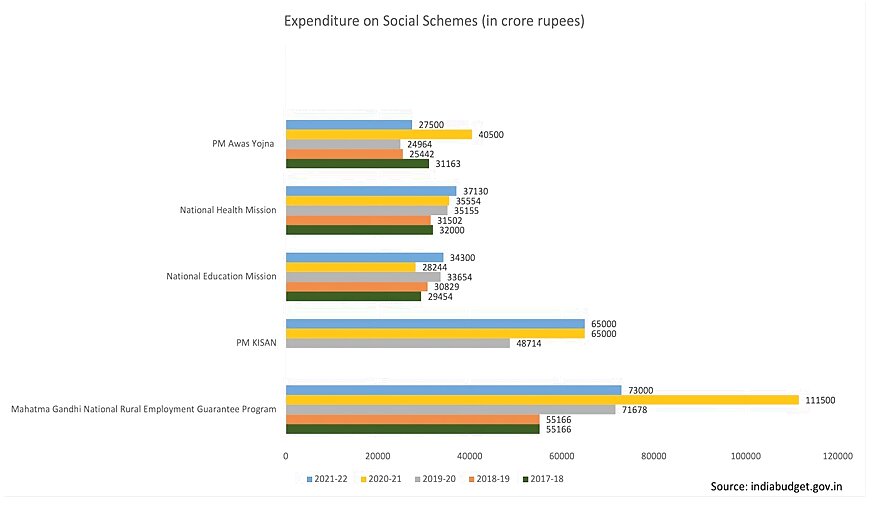

The acceptance of higher deficit and restoring systems to normal is the first step to any economic recovery; this could only be done by the rebuilding of broken lives and shattered balance sheets, and giving time and reprieve for businesses to help them recover. Hence, the loan moratoriums that were announced during the year for corporates over the year in different stimulus packages that were almost mini-budgets. Each one of them tackled some aspect of the restoration process such as liquidity for small and mid- corporates, and wages and livelihoods for informal, migrant and gig workers; schemes such as MNREGA that offered assured employment for migrant workers in the rural areas were scaled up beyond their budgetary allocations, ballooning to Rs 1,18,000 crore.

More significantly, the importance of healthcare infrastructure and services has now been accepted as an important and urgent component of the restoration process. Expenditure on it has been increased 137% to Rs 2,23,840 crore from Rs 94,450 crore a year ago. Healthcare services especially during Covid times threw major systemic lacunae not just in terms of handling the pandemic but in terms of systemic deficiencies. While successive committees and reports have talked about increasing healthcare expenditure to 2.5% it has never acquired the importance or urgency that has been forced by the pandemic. The current expenditure, though not sufficient, is the biggest hike seen in decades. If implemented methodically and efficiently, it will help create health hubs, a centre for fighting infectious diseases, and virology research centres. Hearteningly, a part of this Budget will also be spent towards creating holistic wellness in the form of better access to water and waste segregation infrastructure. Urban Swachh Bharat Mission also gets an allocation of Rs 1,41,678 crore.

What Gets How Much

REVIVE

While the budget is a revenue-and-expenditure document, the FM’s speech is expected to provide an overall view of the policy framework. This time the focus has been on policies that would help revive systems, processes and institutions.

Public-sector companies have always been a bane of the government when it comes to efficiency, capital utilisation, and delivery. Hence the PSE policy was announced before the Budget; now the crucial need is to execute divestment, monetisation and privatisation. By past learnings, the practical way forward is to move fast with smaller successes and build them up to meet the target of Rs 1,75,000 crore set for receipts. This is not going to be achieved by selecting companies like Air India which have just a few buyers and a huge debt overhang, but is likely to work for existing listed companies faster, especially companies where the government has minor stakes and is just holding on to them for vicarious reasons.

Monetisation of assets like road projects with NHAI is a low-hanging fruit and may be possible if the toll guarantees given on these projects are backed by sovereign guarantees, as there have been enough instances of toll contract granted to concessionaires being cancelled by the government and courts. The finance minister also talked about the monetisation of the land bank lying with various CPSE, state government and other government organisations. This may revive the non-tax receipts of the government currently targeted at Rs 2,43,000 crore.

Several sectors are looking for revival or stimulus boost; during the course of the previous year, the FM announced several packages. The industry was eagerly awaiting the allocation the government would make to follow-up these stimulus announcements, one of the most important being production-linked incentive for the manufacturing sector.

She announced that the government aims to spend ₹1.97 lakh crore on various PLI schemes over the next 5 years, starting from this fiscal. This will be in addition to the ₹40,951 crore announced for the PLI for electronic manufacturing schemes.

To incentivise the country’s start-ups, the eligibility for claiming tax holidays for start-ups has been increased by one more year, until March 31, 2022. A slew of incentives for building, selling and buying affordable homes have been extended to the same date.

A new voluntary scrapping policy will soon be announced; that will give a strong nudge to demand creation in the auto-sector and help its revival. More projects have also been added to the National Infrastructure Pipeline. To fund long-term projects the government also plans to amend the law to set up a new DFI, a reversal of a two decades-old policy. Specialised term-lending DFIs such as IDBI and ICICI turned into banks and left a huge void in the market for project-based financing; it also led to concentration of funding among a few promoters and families. Now the FM has allocated Rs 20,000 crore to capitalise a new DFI.

To ensure credit grows and reaches the right borrowers it is also important to issue differentiated banking licenses for MSME, logistics and custodian sectors.

Even for the International Financial Services Centre (IFSC) being set up in GIFT City, it is important that the full ecosystem of financial institutions is created there to include custodian banks. While the FM has announced a revision of the tax holiday and allowed foreign banks to set up shop in the IFSC, it is important to also allow Indian custodian banks in GIFT City. This will create a level playing field between Indian custodians and foreign banks in keeping with the spirit of Atmanirbhar Bharat.

Incoming

RESURGE

The resurgence will happen when existing capacity is utilised; for that demand has to grow as most Covid-induced supply chain constraints have been removed .

They only remain for a few sectors in the services industry such as restaurants or other contact-based services. But demand is important–it’s not only a matter of money supply, but also confidence in future earnings.

Discretionary spending will only rise once the fear of COVID goes away and consumers are fully vaccinated. Given that the vaccination for the bulk of the population to create herd immunity is still 12 to 18 months away, it is important that the animal spirits of entrepreneurship are boosted. While a large section of naysayers including former governors find the stock market suspect, it is a truism that the market moves at least 6-9 months in advance of fundamental growth.

This means that foreign funds are discounting the growth that will come after two to three quarters. While there may be irrational exuberance in the stock market, the global liquidity flows in the low interest rate world will command higher valuation for growth. The response of the BSE Sensex after the Budget was remarkable; it went up by 5% and stocks like State Bank of India responded admirably, the sectoral Bank NIFTY Index was an outperformer. When NPA-laden banks start performing in a low credit growth market it means that the investors are taking a bet on the whole economy and not taking a sectoral view of things

Hence, it is important to mention here that the FM has been wise in ‘not’ taking some decisions, like imposing a wealth tax or a tax on stock market gains. The bad ideas that were floating around before the Budget have been wisely rejected by the FM.

The battles that you don’t fight are as important as the battle you chose to fight.

(K Yatish Rajawat is a public policy expert, who tweets at @yatishrajawat. Views expressed are personal.)

Read all the Latest News, Breaking News and Coronavirus News here

Comments

0 comment