- Use the formula V = P x (1 + R) ^ n, where V is the maturity value, P is the principal amount, n is the number of compound intervals, and R is the periodic interest rate.

Determining The Maturity Value

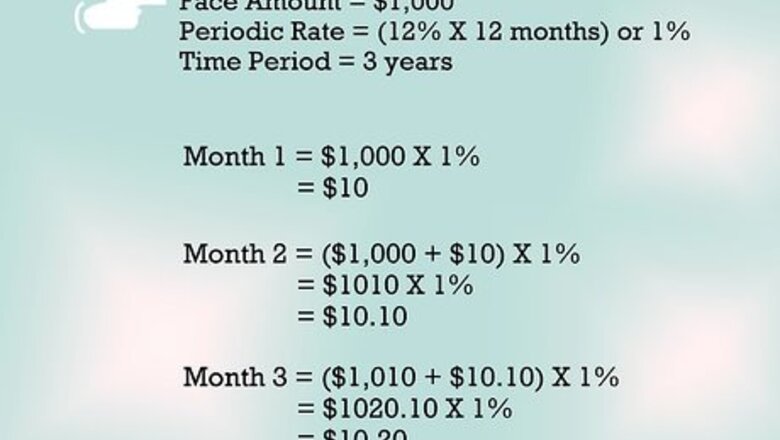

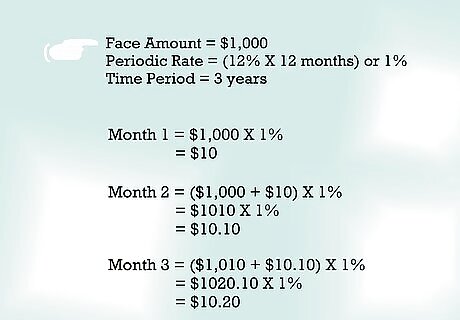

Use the periodic rate to compute your interest earned. Assume that you own a $1,000 12% certificate of deposit that matures in 3 years. Your CD pays all of the interest at maturity. To compute the maturity value, you need to calculate all of your compounding interest. Say that your CD compounds interest monthly. You periodic rate is (12% / 12 months = 1%). To keep it simple, assume that each month has 30 days. Many investments, including corporate bonds, use a 360-day year to calculate interest. Assume that January is the first month that you own the CD. In month one, your interest is ($1,000) X (1%) = $10. To calculate interest for February, you need to add the January interest to your principal amount. Your new principal amount for February is ($1,000 + $10 = $1,010). In February, you earn interest totaling ($1,010 X 1% = $10.10). You see that your February interest is higher than January’s amount by 10 cents. You earn additional interest because of compounding. Each month, you add all of the prior interest to the original $1,000 principal amount. The total is your new principal balance. You use that balance to calculate interest for the next period (a month, in this case).

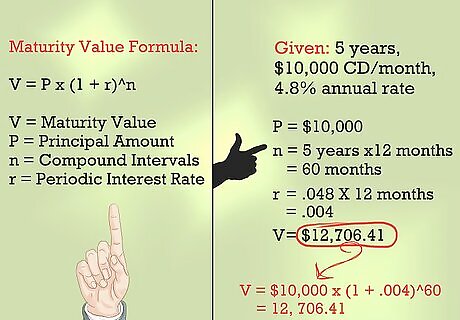

Apply a formula to quickly calculate maturity value. Rather than compute compounding interest manually, you can use a formula. The maturity value formula is V = P x (1 + r)^n. You see that V, P, r and n are variables in the formula. V is the maturity value, P is the original principal amount, and n is the number of compounding intervals from the time of issue to maturity date. The variable r represents that periodic interest rate. For example, consider a 5-year, $10,000 CD compounded monthly. The annual interest rate is 4.80 percent. The periodic rate (the r variable) is (.048 /12 months = .004). The number of compounding periods (n) is calculated by taking the number of years in the security and multiplying by the frequency of compounding. In this case, your can compute the number of periods as (5 years X 12 months = 60 months). The variable n equals 60. The maturity value, or V = $10,000 times (1 + .004)^60. The maturity value V works out to $12,706.41.

Search for an online maturity value calculator. Find an online calculator for maturity value using a search engine. Make your search specific to the security you are valuing. If you own a money market fund, for example, type in "money market fund maturity value calculator". Search for a reputable site. The quality and usability of each online calculator tool can vary greatly. Use two different calculators to validate your results. Input your information. Enter the data from your investment or proposed investment into the calculator tool. This will include the principal, annual rate of interest and the duration of the investment. It may also include the frequency of compounding for the investment. Check the result. Make sure that the maturity value makes sense. To verify that the maturity date is reasonable it probably makes sense to confirm the result in another online tool.

Reviewing Debt Instruments

Go over the features of a bond. A bond is issued to raise money for some purpose. Corporations issue bonds to raise money to run the business. Government entities, such as a city or state, may issue a bond to pay for a project. A municipality may issue a bond to build a new public swimming pool, for example. Every bond is issued with a specific face amount. The face amount of the bond is the amount an investor receives at maturity. The maturity date of a bond is the date that the issuer must repay the face amount. In some cases, the face amount and all of the interest earned is repaid on the maturity date. All of the details of the bond are listed on a bond certificate. Today, bond certificates are issued in electronic form. Investment professionals refer to this electronic format as book entry form. The face amount and maturity date are listed on the book entry document, along with the interest rate. If you buy a $10,000 6% IBM corporate bond due in 10 years, for example, all of those details will be listed on the electronic bond certificate.

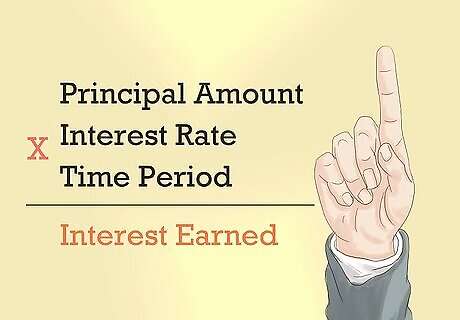

Consider the amount that you receive on the maturity date. Most corporate bonds pay interest semi-annually. At maturity, you receive the face amount of the bond. Other debt instruments, such as certificates of deposit (CDs), pay the face amount and all of the interest at maturity. Another term for the face amount is the principal. The formula to calculate interest earned is (principal amount multiplied by interest rate multiplied by time period). The annual interest for the IBM bond is ($10,000 X 6% X 1 year) = $600. If all of the interest was paid at maturity, the first year’s interest of $600 would not be paid until the end of 10 years. In fact, each year’s interest would be paid at the end of 10 years, along with the face amount (principal).

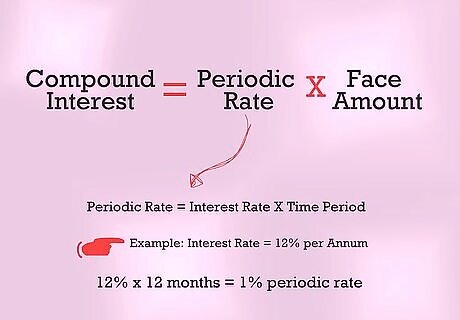

Add in the impact of compounding. Compounding means that the investor earns interest on both the face amount of the debt instrument, and any prior interest earned. If your investment pays all of the interest at maturity, you will probably earn compounding interest on your past interest earnings. The periodic rate is the rate of interest you earn for a particular time period, such as a day, week or month. To calculate compounding interest, you need to determine the periodic rate. Assume that your investment earns 12% interest annually. Your interest compounds monthly. In this case, your periodic rate is (12% / 12 months = 1%). To compound interest, you multiply the periodic rate by the face amount.

Comments

0 comment